This article originally appeared on Mongabay here.

The recent forest fires in Brazil and Bolivia showed once more that traditional approaches to sustainable development and nature conservation are not sufficient to reduce carbon emissions from land use and stop the ongoing destruction of natural resources.

Innovative solutions are needed and Forest Landscape Restoration (FLR) has emerged as a promising alternative holistic concept to improve rural livelihoods and at the same time halt and reverse forest and land degradation, thereby storing additional carbon in trees and soil.

Thanks to these outcomes, FLR is also an appropriate approach to achieve certain UN Sustainable Development Goals, in particular those related to Goal 13 – Climate action: “Take urgent action to combat climate change and its impacts by regulating emissions and promoting developments in renewable energy”; and Goal 15 – Life on land: “Protect, restore and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, and halt and reverse land degradation and halt biodiversity loss.”

“Governments acknowledge the nexus between climate change, land degradation, decreased agricultural production, conflicts and migration, and have started to implement FLR,” says Dr. Paola Agostini from the World Bank, “which is reflected in a sharp increase of the forest and landscape portfolio from $1.8 billion in 2016 to $2.5 billion in 2018.”

But Forest Landscape Restoration requires major investments that exceed the budgets of national governments, international donors, and multilateral development banks. To address these investment gaps, help from the private and financial sector is needed, and this is where sustainable finance comes into play. Sustainable finance includes a variety of financial mechanisms, instruments, and products that aim to deliver environmental and social benefits combined with a financial return.

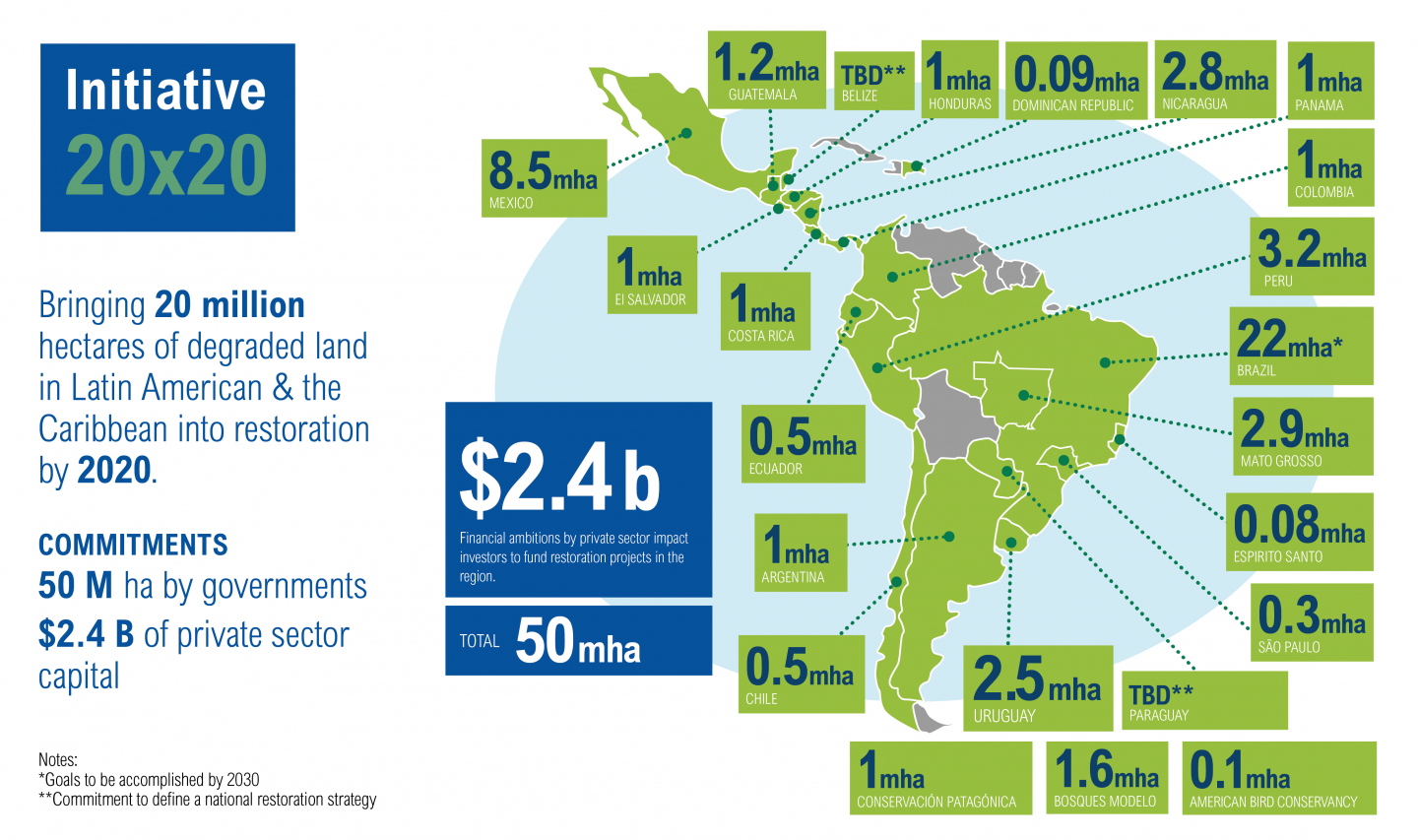

An example of sustainable finance in FLR is the country-led Initiative 20×20, which strives to restore 50 million hectares (about 124 million acres) of degraded lands in Latin America and the Caribbean. A group of impact investors, private companies, investment advisors, and private funds have pledged over $2 billion for projects in support of Initiative 20×20 countries’ restoration commitments. Despite this large sum, little progress has been made on the ground and FLR projects are not reaching scale. To get a better understanding of how sustainable finance works in practice, various financial and technical partners of the initiative and two multilateral development banks were interviewed by the International Center for Tropical Agriculture (CIAT) and asked about the bottlenecks they encounter and how they respond to them. (Full disclosure: I helped conduct the interviews when I worked at CIAT. The results have not been published elsewhere.)

A major bottleneck among investors in Initiative 20×20 is project design and management. Not all participating countries have adequate capacity to develop a landscape plan with an investment component and find the different flavors of capital — equity, working capital, loans, grants – needed to support it, and to implement projects at scale.

“It is all about partnerships,” comments Eduardo Tugendhat of Palladium, an investment platform that triangulates producers, buyers and the financial sector. “Help farmers that need to collaborate by developing a business plan. Link these cooperatives with local players that are interested in the products, but that do not have sufficient capital. Then find funds or financial instruments to finance the partnership.”

However, “there is a lot of mistrust among the private sector, government and communities, which hinders the building of coalitions. To create a public-private-civic partnership requires time and is a process with many steps,” says Shaun Paul of Ejido Verde, a triple bottom line, sustainable pine resin company.

Other bottlenecks, according to Kaspar Wansleben of the Forestry and Climate Change Fund, are that “the concept of impact investment in landscape restoration is still in its infancy. There are no successful business models and, at the moment, it is mainly trial and error. The sums that impact investors want to invest are too big and the producers cannot offer an attractive financial product.”

Moreover, “both public and private investors want to know what to expect and want to see results in the short-term, which is not always feasible with natural assets that will only start generating revenues in the long-term,” says Bruno Mariani of Symbiosis Investimentos. “This means that,” Camille Rebelo of Ecoplanet Bamboo argues, “most financial institutes perceive these investments as too risky and although everybody agrees that innovative solutions are needed, nobody wants to invest in a new product that has not established a market price yet.” Elizabeth Teague of Root Capital adds that “due diligence entails high costs in emerging markets, meaning impact investors often must accept below-market returns to reach their target borrowers.”

To increase investors’ willingness to write checks, public-funded grants play a crucial role:

- First, by funding accelerators that finance the setup and costs of raising capital to get to the first close, i.e. when a fund has sufficient legal commitments to start investing and making deals;

- Second, by funding technical assistance facilities to improve investment readiness;

- Third, and most importantly, by providing financial guarantees with public capital that is willing to share the risks and take first loss. Other ways for companies to overcome investor reticence are through self-financing or the use of hybrid models where investment capital is merged with philanthropy, but both strategies limit the ability to scale the investment.

“The business model of multilateral development banks is based on their triple-A rating, which causes them to operate risk averse. Therefore, they are not willing to offer financial guarantees for impact investors in FLR,” says Martin Berg of the European Investment Bank. “Instead, governments should provide these by converting their grants into financial instruments.” However, a reallocation of public funds in favor of the private and financial sector will certainly induce the indignation of traditional recipients of funding and will face opposition from donors, many of whom believe that the private sector must take care of itself and should not be supported with public money to make a profit.

The Global Impact Investing Network (GIIN) estimates that less than 4 percent of assets under management worldwide are related to sustainable finance. Institutional investors have access to the largely untapped traditional capital markets, but to get them on board, sustainable finance must mature, providing proven track records and creating recognizable patterns so investors can better understand and price risk.

Eventually, if the ambitious goals of Initiative 20×20 or the Sustainable Development Goals are to be met, all capital must be engaged, whether it’s private, public, or philanthropic.

The following persons and companies, institutes and NGOs are thanked for their collaboration: Terra Global Capita; Hans Loth, Rabobank; Nanno Kleiterp, &Green Fund, Kaspar Wansleben, Forest and Climate Change Fund; Lenny Martinez & Irene Montes, 12Tree; Eduardo Tugendhat, Palladium Group; Julie Reneau, Nespresso Sustainability Innovation Fund; Richard Ambrose, Pomona Impact; Shaun Paul, Ejido Verde; Camille Rebelo, Ecoplanet Bamboo; Paola Agostini, World Bank, Efrain Peña & Leonardo Saenz, Permian Global; Martin Berg, European Investment Bank; Bruno Mariani, Symbiosis Investimentos; Werner Thorne, Oikocredit; Elizabeth Teague, Root Capital; Oriane Plédran, Moringa Investments; Rianne van der Bom, Progreso; Daniele Mariuzzo & Ted van de Put, IDH; and Luis Salgado, Canopy/Ecotierra.

The study was funded by USAID's Global Climate Change Program.